Business

Breaking free from conventional investment paths; How to make your money work harder – Part II

Contineud from Yesterday

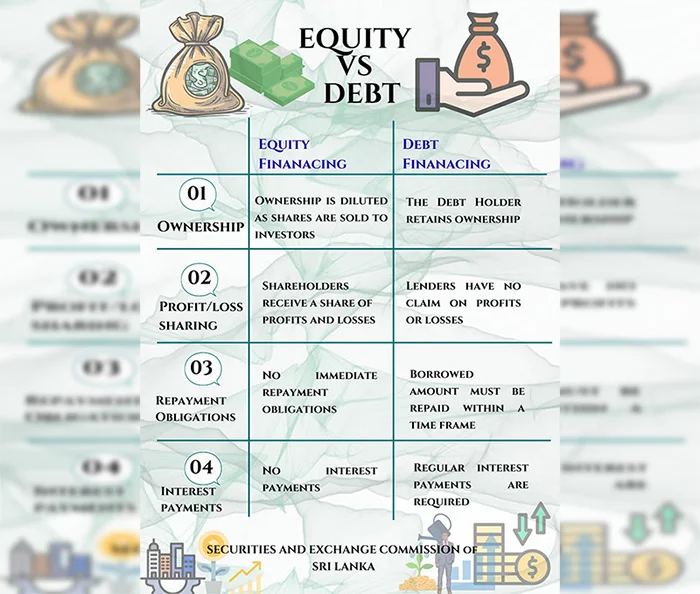

Repayment obligations – No immediate repayment obligations in equity financing. In debt financing however, the borrowed amount must be repaid within a time frame.

Interest payments – In terms of equity financing, there are no interest payments but in debt financing regular interest payments are required.

Debentures Decoded: The Company IOU System

Debentures are essentially formal IOUs that companies give you when you lend them money. What makes them particularly attractive to investors is their predictable nature and security features. They offer fixed returns, meaning you know exactly how much you’ll earn or can predict your return with certainty. Most debentures provide regular income through interest payments made every six months, creating a steady cash flow for investors. Each debenture comes with a specific maturity date when the company must repay the full principal amount you originally lent them. Perhaps most importantly, debenture holders enjoy priority treatment in the company’s capital structure, which means if the company faces financial difficulties, debenture holders get paid before shareholders, providing an additional layer of security for your investment.

The Flip Side: What Could Go Wrong?

Like any investment, debentures come with risks:

Interest Rate Risk – When interest rates rise, existing bond prices fall since newer bonds offer higher yields. Long-term bonds are more sensitive to rate changes than short-term ones. This creates potential capital losses if you need to sell before maturity.

Credit Risk – The borrower may default on interest payments or fail to repay the principal. This is particularly relevant to corporate bonds, high-yield bonds, and emerging market debt. Even government bonds aren’t immune, as sovereign defaults can occur.

Inflation Risk – Fixed-rate debt investments lose purchasing power when inflation exceeds the bond’s yield. Your real return (after inflation) may be negative even if you receive all promised payments.

Liquidity Risk – Potential difficulty in buying or selling a bond at a fair price, especially during periods of market stress. This risk arises because some corporate bonds may have fewer buyers and sellers compared to government bonds, making it harder to execute trades quickly without impacting the price significantly.

Event Risk Corporate restructuring, mergers, natural disasters, or regulatory changes can suddenly impact a borrower’s ability to service debt, even for previously stable issuers.

Prepayment Risk Borrowers may pay off debt early when interest rates fall, forcing you to reinvest at lower rates. This is common with mortgage-backed securities and callable bonds.

Tips on How To Balance The Devil On Your Shoulder; Guide to Risk Management

Build bond ladders with staggered maturities to reduce timing risk and provide regular reinvestment opportunities. Shorter-duration bonds (under 5 years) are less sensitive to rate changes. Consider floating-rate bonds that adjust with interest rate movements.

Diversify across multiple issuers, sectors, and credit ratings rather than concentrating in single borrowers. Research credit fundamentals and consider professional credit analysis for corporate bonds.

The Array of Debt Securities Facilitated; Invest In What You Believe In

The Securities and Exchange Commission of Sri Lanka serves as both the gatekeeper and facilitator of bond investments. Acting like a financial referee, the SEC creates rules and approval processes that allow companies to borrow money from the public through bonds while protecting investors from fraud and misinformation. Their dual role as regulator and facilitator has enabled the development of innovative bond markets, ensuring that when companies want to issue bonds, they must provide complete and honest information about their finances and intentions. Through this careful oversight and facilitation, the SEC has made possible the following bond categories that serve both investor returns and broader societal goals:

Corporate Promises of Economic Affluence: Corporate Bonds

The corporate bond market presents a fascinating risk-reward spectrum. At one end, bonds offered from established corporations with good credit ratings offer reliable returns slightly higher than government securities. At the other end, high-yield or “junk” bonds from less financially stable companies entice investors with premium interest rates to compensate for elevated risk.

The corporate bond market offers remarkable diversity, allowing investors to precisely calibrate their desired balance between safety and yield.

Save the Planet and Make Profit: Unlocking Value Through GSS+ Bonds

GSS+ refers to a category of financial products designed to fund projects with positive environmental and social impacts. The Regulatory Framework for listing and trading the following Bond categories have been enabled at the CSE:

Green Bonds – Green Bonds debt securities specifically designed to fund projects with positive environmental or climate benefits.

Blue Bonds – Blue Bonds are debt securities designed specifically to finance projects related to ocean conservation and sustainable marine activities.

Social Bonds – Social Bonds are debt securities that raise funds specifically for projects delivering positive social outcomes and addressing social challenges. They offer investors a way to generate financial returns while supporting social welfare initiatives.

Sustainability Linked Bonds – Sustainability Linked Bonds differ from the other types of GSS+ Bonds in that their proceeds are not used to finance specific projects but are instead made available for general corporate purposes, with the issuer contractually undertaking to achieve predefined, measurable sustainability targets or Key Performance Indicators (KPIs).

“Faith-Based Finance Finds Home”: Shariah-Compliant Debt Securities

Shariah compliant Debt Securities, commonly known as Sukuk, represent Shariah-compliant financial certificates that embody partial ownership in an underlying asset, usufruct, service, project, business, or investment. Unlike conventional bonds that create debt obligations with interest payments, sukuk are structured as investment certificates that provide returns derived from asset performance rather than interest.

Enabling this product at the CSE is expected to attract previously untapped capital by opening doors to foreign portfolio investments from Shariah seeking investors.

Sri Lanka’s Blooming GSS+ and Faith-Based Bond Market

DFCC Bank Pioneers Green Bond

Sri Lanka’s first Green Bond was issued by the DFCC Bank in September 2024 for a total value of LKR 2.5 billion at a coupon of 12%.

This issue was oversubscribed. In December 2024, the DFCC went on to obtain a dual listing for its Green Bond at the Luxembourg Stock Exchange (LuxSE).

Alliance Finance Issues LKR One Billion Worth of Green Bonds

Alliance Finance Company PLC, a Non-Banking Financial Institution (NBFI) issued LKR 1 billion of Green Bonds in February 2025 at a coupon of 10.75%, which was also oversubscribed.

Sri Lanka’s First Ever Faith Based Bond

Vidullanka, a renewable energy company pioneering Rs. 500 m Sukuk issue (Compliant with Shariah Law) was oversubscribed on the opening day itself.

More GSS+ investment opportunities on the horizon

Several other corporate entities such as Resus Energy PLC and Sarvodhaya Development Finance are in the pipeline for issuing GSS+ Bonds.

“Building Tomorrow Today”: Infrastructure Bonds

The introduction of Infrastructure Bonds marks a significant step toward addressing the nation’s infrastructure financing gap. These specialized debt instruments will channel private capital into critical projects spanning transportation, energy, water, and digital infrastructure.

With extended maturities designed to match the long-term nature of infrastructure assets, these bonds offer investors stable, predictable returns while contributing to national development priorities.

Infrastructure Bonds will create a win-win scenario where investors gain exposure to essential assets with inflation-protected returns, while the country benefits from accelerated infrastructure development.

Capital Fortified: Unlocking value through Basel III Tier 2 Instruments

Basel III-compliant debentures represent a specialized category of debt instruments that adhere to the regulatory standards established by the Basel Committee on Banking Supervision in response to the 2007-2008 global financial crisis. These debentures are designed to strengthen bank capital requirements, stress testing, and market liquidity risk management.

“Endless Opportunities”: Perpetual Bonds

True to its name, Perpetual Bonds are debt securities with no maturity date and pays interest indefinitely. These instruments offer unique advantages for both issuers seeking stable long-term funding and investors looking for consistent income streams.

Unlike conventional bonds, perpetuals remain outstanding until the issuer chooses to redeem them, typically after a specified initial period.

Perpetual Bonds represent financial innovation at its finest. They provide corporates with quasi-equity financing without diluting ownership, while investors benefit from higher yields compared to traditional fixed-income products.

“Higher Risk, Higher Reward”: High-Yield Bonds

Rounding out the new offerings are High-Yield Bonds, sometimes known as “junk bonds,” which carry higher interest rates to compensate for their greater risk profile. These instruments typically come from issuers with lower credit ratings or newer enterprises without established credit histories.

Market participants have welcomed the addition, noting it completes the CSE’s fixed-income ecosystem by catering to investors with more aggressive risk appetites.

High-yield bonds fill a crucial gap in our market. They offer potentially attractive returns in a low-interest environment and provide companies that might not qualify for investment-grade ratings with vital access to capital. Currently this is facilitated for entities regulated by the CBSL or the Insurance Regulatory Commission of Sri Lanka (IRCSL)

Why Capital Markets Matter: The Win-Win Story

For Companies Raising Money:

Cheaper Funding: Instead of paying high bank interest rates, companies can often raise money more cheaply through capital markets.

No Collateral Hassles: Unlike bank loans that require mortgaging property, companies can raise funds based on their business prospects.

Flexibility: They can choose between giving away ownership (equity) or borrowing (debt) based on their needs.

Growth Capital: Access to large amounts of money helps companies expand, hire more people, and in turn contribute to economic growth.

For Everyday Investors:

Better Returns: Instead of earning a lesser return from bank deposits, you might be able to earn significantly higher returns in the capital market

Choice and Control: You decide which companies to support with your money.

Wealth Building: Over time, successful investments can significantly grow your wealth.

Economic Participation: You become part of Sri Lanka’s economic growth story.

The Bigger Picture: Building Tomorrow’s Sri Lanka

Capital markets aren’t just about making money – they’re about building the future. When you invest in a renewable energy company’s debenture, you’re funding clean power for Sri Lanka. When you buy shares in a tech startup, you’re supporting innovation and job creation.

Getting Started: Your First Steps

Ready to explore capital markets? Start small:

Learn the basics through free regulatory sources like Securities and Exchange Commission of Sri Lanka

Open a trading account with a licensed stockbroker

Start with blue-chip companies – established firms with good track records

Diversify your investments – don’t put all eggs in one basket

Think long-term – capital markets reward patience

Still feeling apprehensive? Try Unit Trusts.

Unit Trust Funds are a collective investment scheme that is a pooling vehicle of your funds, offering professionally managed investment pools with various risk profiles suitable for unsophisticated investors.

Minimum investment begins from as low as LKR 1,000.00. Risk level varies based on type of the Scheme who creates a diversified portfolio based on the fund’s parameters to earn a return.

Then your money is used by professional fund managers who know what they’re doing. They take everyone’s money and buy a mix of different investments – like shares in companies, government bonds, and other financial assets.

Steps to follow;

Choose a licensed managing company and open a unit trust account

Open your account with as little as Rs.1000

Choose the Scheme – Once your account is open, you need to choose a fund to invest in. You can choose from a range of funds such as Growth funds, Income funds, Balanced funds, Money Market funds, Sector Funds and Index Funds. Each fund has different risks and returns, so you need to decide which is the best fit for your goals and risk appetite.

Monitor your investment

The beauty of unit trusts is their simplicity – investors receive the benefit of professional management without needing to be a financial expert.

Finally, it’s important to remember, all investments carry risks. Never invest money you can’t afford to lose and always do your homework before making investment decisions.

Capital markets have democratized finance in Sri Lanka, giving everyone a chance to participate in the country’s economic growth, offering opportunities to grow your wealth while supporting businesses that create jobs and drive progress.

To be Continued

by Securities and Exchange Commission

of Sri Lanka

Nestlé Lanka Limited this year marks 120 years of operations in Sri Lanka, highlighting a century-long presence that has extended beyond food manufacturing to supporting farmers, communities, youth employment and environmental sustainability.

Established in 1906, the company has grown into one of Sri Lanka’s leading food and beverage manufacturers, today producing more than 90% of the products it sells locally. Over the decades, Nestlé Lanka has built a strong domestic footprint through local sourcing, long-term farmer partnerships and continued investment in manufacturing.

Through widely recognised brands such as Nestomalt, Milo and Maggi, the company has become a familiar presence in Sri Lankan households, offering products designed to meet local nutritional needs. Many of its products are fortified with micronutrients aimed at improving dietary intake, while brands such as Milo and Nestomalt have also supported youth sports and active lifestyles in the country.

Nestlé Lanka’s engagement with local agriculture has also played a role in strengthening rural livelihoods. The company works closely with dairy and coconut farmers, providing technical assistance, skills development and reliable market access as part of its responsible sourcing efforts.

The company has also expanded programmes aimed at improving youth employability. Through the “Nestlé Needs YOUth” initiative, young Sri Lankans are provided with access to training, learning and career opportunities. Partnerships with organisations such as BConnected have also helped promote inclusive employment opportunities for people with disabilities.

Sustainability has become an increasingly central focus of the company’s operations. Nestlé Lanka’s manufacturing facility in Kurunegala operates on 100% renewable electricity, while a biomass boiler commissioned in 2024 has helped reduce carbon emissions from manufacturing. The company aims to achieve net-zero carbon emissions by 2050.

Efforts to reduce environmental impact have also extended to packaging. Nestlé Lanka pioneered the shift from plastic to paper straws in aseptic beverage cartons in 2019 and supported the establishment of Sri Lanka’s first recycling plant for such cartons. The company aims to become fully plastic neutral by 2026.

Chairman and Managing Director Bernie Stefan said the milestone reflects the long-standing trust Sri Lankan consumers have placed in the company and the partnerships it has built across the country over generations.

By Sanath Nanayakkare

The Ceylon Chamber of Commerce has formally handed over its historical records to the National Archives Department of Sri Lanka, placing over a century of the nation’s commercial history into the care of the country’s official custodians of heritage.

The historical archive being handed over spans from the Chamber’s founding in 1839 to 1973, and includes correspondence, meeting minutes, reports, ledgers, and publications that chronicle the development of trade, enterprise, and industry in Sri Lanka. Together, these records provide a rare and detailed account of how the island’s economy evolved and how its business community helped shape national progress.

The Ceylon Chamber of Commerce was established on 25 March 1839 on the principle that the interests of commerce and trade are best advanced when merchants unite and cooperate in matters affecting the common good. At the time, Ceylon was among the earliest regions in Asia to establish a chamber of commerce, alongside counterparts in Bengal, Bombay, Madras, Canton, Penang, and Singapore.

From its earliest years, the Chamber played a central role in organising and guiding trade. It played a central role in establishing and growing the export economy built on commodities such as coffee, cinnamon, coconut oil, tea, and rubber, and hosted the island’s renowned tea and rubber auctions. It also developed rules and standards for trading practices, helping create an environment of trust and reliability that enabled Sri Lanka’s commerce to thrive.

Ceylinco Life has secured two prestigious accolades for its 2024 Annual Report, reaffirming the Company’s leadership in transparent, accountable and sustainability-driven corporate reporting.

At the Association of Chartered Certified Accountants (ACCA) Sri Lanka Sustainability Reporting Awards, Ceylinco Life emerged winner in the ‘Other Financial Services’ category for the second time. Organised by the ACCA, one of the world’s most respected professional accounting bodies, the awards are assessed against globally accepted sustainability and reporting standards rather than local benchmarks, lending them strong international credibility. The recognition underscores Ceylinco Life’s sustained commitment to setting new benchmarks in sustainability reporting within Sri Lanka’s corporate sector.

The Company’s reporting excellence was also recognised at the TAGS Awards 2025 presented by the Institute of Chartered Accountants of Sri Lanka (CA Sri Lanka). Ceylinco Life was ranked among the Top 10 Integrated Reports in Sri Lanka and received the Silver Award in the Insurance Companies category for entities with Gross Premium above Rs. 10 billion. The TAGS Awards evaluate annual reports on the pillars of Transparency, Accountability, Governance and Sustainability, and are widely regarded as Sri Lanka’s benchmark for corporate reporting excellence.

Commenting on the significance of the recognitions, Ceylinco Life Senior Executive Director/ Chief Financial Officer Mr Palitha Jayawardena said these awards validate the Company’s disciplined approach to transparency, governance and sustainability. “Our integrated reporting journey is not only about compliance; it is about clearly demonstrating how we create and protect value over the long term. Being recognised both by the ACCA and by CA Sri Lanka affirms that our reporting standards meet the highest expectations and reflect the depth of our commitment to responsible and sustainable business practices,” he said.

Advisory for Severe Lightning issued to the Western and Sabaragamuwa provinces and Galle and Matara districts

Jemimah Rodrigues, Harmanpreet Kaur, Mitchell Starc and Kuldeep Yadav among ESPNcricinfo award winners for 2025

China approves ‘ethnic unity’ law requiring minorities to learn Mandarin

Nasa spacecraft weighing 1,300lb due to re-enter Earth’s atmosphere

Chinese national arrested over attempt to smuggle 2,000 queen ants from Kenya

Attacks reported on three more cargo ships in Gulf, with oil price back near $100

‘Dates have the highest sugar content to fight Coronavirus’

Sunday Island 27 December – Headlines

#SundayIsland 17th December – Headlines

Sunday Island – 28th March

Sunday Island Headlines – 21 March

Sunday Island – 21st February – Headlines

-

News7 days ago

News7 days agoUniversity of Wolverhampton confirms Ranil was officially invited

-

News6 days ago

News6 days agoPeradeniya Uni issues alert over leopards in its premises

-

News7 days ago

News7 days agoFemale lawyer given 12 years RI for preparing forged deeds for Borella land

-

News4 days ago

News4 days agoRepatriation of Iranian naval personnel Sri Lanka’s call: Washington

-

News7 days ago

News7 days agoLibrary crisis hits Pera university

-

News6 days ago

News6 days agoWife raises alarm over Sallay’s detention under PTA

-

News7 days ago

News7 days ago‘IRIS Dena was Indian Navy guest, hit without warning’, Iran warns US of bitter regret

-

Latest News7 days ago

Latest News7 days agoSri Lanka evacuates crew of second Iranian vessel after US sunk IRIS Dena