Opinion

‘Bad Boy Billionaires’ of Sri Lanka

By UPALI COORAY

This headline quotation in part, is the title of a Netflix series “Bad Boy Billionaires”. This Netflix series brings out some of the epoch-making financial scams in India. The documentary film exposes the truth in an investigation in major corruption scandals, money laundering in India involving Vijay Mallaya (Kingfisher Airlines) Subrata Roy (Sahara India) Nirav Modi (Gitanjali group) Ramalinga Raju (Sathyamgani computers)

Among these scammers Subrata Roy has done something which has parallels in Sri Lanka.

India’s market regulator petitioned the Supreme Court to direct tycoon Subrata Roy to an immediate payment of 626 billion rupees ($8.4 billion) meant for poor investors.

The Securities and Exchange Board of India said the outstanding liability of the Sahara India Parivar group’s two companies and the conglomerate’s chief Roy stand at 626 billion rupees, including interest, according to court filings.

India’s Supreme Court in 2012 ruled that Sahara group of companies violated securities laws and illegally raised over $3.5 billion. The companies said monies were raised in cash from millions of poorest of the poor of Indians who could not avail banking facilities. SEBI could not trace the investors and when Sahara firms failed to pay up, the court sent Roy to jail.

Roy, who at different times owned an airline, Formula one team, cricket team, plush hotels in London and New York, and financial companies, stayed in jail for over two years and has been out on parole since 2016.

The Sahara story, almost a decade after the final judgment, is far from over. Roy has so far deposited over 150 billion rupees, SEBI said in the court filing, while the Sahara group said it had deposited 220 billion rupees.

Financial scams in our country have increased in recent times and not a day passes without news of customers being cheated by finance companies, etc. Let’s start with the oldest of Sri Lankan con- artistes Emil Savundra or Emil Savundranayagam, who was a Sri Lankan who settled down in Britain in 1960, a born cheat. The collapse of his Fire, Auto and Marine Insurance Company left about 400,000 motorists in the United Kingdom without cover.

As a post-war bootlegger, Savundra committed bribery and fraud on an international scale before settling down in the UK to sell low-cost insurance in the fast-growing automotive market. By defaulting on mandatory securities, he funded a lavish lifestyle and travelled in fashionable circles even with the famous Christine Keeler and Mandy Rice-Davies. He was into power boat racing too.

This drew scrutiny by the press, which discovered major frauds. In a TV interview with David Frost, Savundra demonstrated contempt for his defrauded customers. The police had been investigating him, and he was soon arrested and sentenced to eight years imprisonment. Released after six, Savundra died two years later as a drug addict.

Piyadasa Ratnayaka alias Danduvam Mudalali of Hungama, Southern province, had allegedly accepted deposits from over 20,000 investors in a pyramid scheme. He was on bail for the alleged financial scam. Mudalali was killed by an unknown armed gang in Pusallawatte, Kuruwita.

Hideki Finance and Investments, which went bust in 1987, had over 4,000 depositors. The Central Bank had to intervene and pay the depositors their dues in instalments.

The multi-million rupee ‘Sakvithi’ scam by Sakithi Ranasingha did not spare even the handicapped or the sick, as it plundered the wealth of thousands of unsuspecting customers who suddenly realised that all their savings had gone up in smoke. About 5,000 investors were defrauded to the tune of 900 million rupees. A Police inspector was also allegedly involved in the scam, which was exposed following a raid by the Central Bank on unregistered financial institutions.

The multi-million rupee ‘Sakvithi’ scam by Sakithi Ranasingha did not spare even the handicapped or the sick, as it plundered the wealth of thousands of unsuspecting customers who suddenly realised that all their savings had gone up in smoke. About 5,000 investors were defrauded to the tune of 900 million rupees. A Police inspector was also allegedly involved in the scam, which was exposed following a raid by the Central Bank on unregistered financial institutions.

Kingsley de Silva, an ex-naval rating suffering from a chronic kidney ailment, has been robbed of Rs. 1.2 million — money he had saved for a life-saving surgery. This money, the 65-year-old Mr. Silva said, included payment he received from the Navy on retirement and the rest from the part-sale of ancestral land in Maharagama. He did not know what to do or whom to turn to.

Dulanjan Atapattu, a retired government teacher was due to undergo heart surgery. He needed extra money for the operation and medication, and invested his savings in what he thought would be an income-generating scheme.

“I invested Rs. 2 million after selling my house. Initially, I got a monthly interest, and was impressed with the return. But I was soon to be proved wrong,”

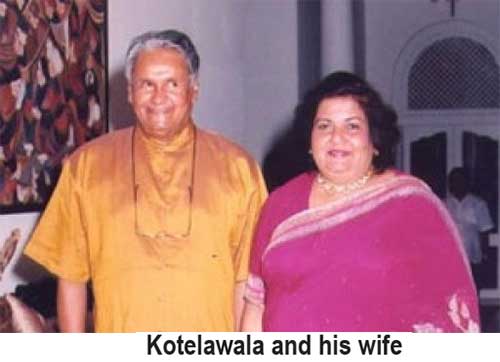

With a self-esteem as philanthropists, embracing the word of God, the very name Deshamanya Dr. Lalith Kotelawala and Lady Dr. Sicille Kotelawala evoked respect, trust and above all a sense of security. That was why 9,054 people in this country, trusted the duo with millions of rupees, in some cases tens of millions of rupees in life savings. Maybe part of those millions belonging to some depositors was black money. Perhaps, some of them invested their money to evade paying tax to the government, or they were just plain greedy or a mixture of both. After all, why did they not invest the monies with financially stable banks?

Whatever the case, they were confident that their savings/loot would be safe in the hands of two human beings held in the highest esteem. There were leading businessmen, civil servants, Buddhist monks, Christian clergy and world-renowned Sri Lanka cricketers, who would never have resorted to money laundering, were also deceived.

When Golden Key collapsed like a pack of cards in December in the year 2008, and as the unsavoury details unraveled in staggered scenes of drama, horrified, dismayed depositors who had been earning as much as 30 and 32 percent on their investments at Golden Key, were forced to come to grips with the fact that soon their monies would be confined to mere numbers on a piece of paper. Soon to be identified as one of the biggest white-collar frauds.

Held in esteem by those who claimed to be his friends and say they trusted him wholeheartedly. Today, these same people spit his name out with vilification. Thousands of families robbed of a monthly interest amounting from thousands to millions of rupees, earned off their capital investment with Golden Key.

At least one depositor from this list, Lady Dr. Sicille Kotelawala will have no such qualms. Her investment in Golden Key was to the tune of Rs. 10.6 million only. A paltry sum by her standards. Even that most likely is what she skimmed off from the company itself. After all, according to court documents she was paid a staggering Rs. 3.5 million a month for being the Deputy Chairperson was just peanuts. She was rich enough not to have to worry about paying for groceries or medicines.

From lower middle-class families to upper, from the rich to the superrich there was no class distinction between the 9,054 people who entrusted their monies with Golden Key.

The strange thing is that most of the big depositors are businessmen who understand finance. They would have known that the unrealistically high interest rates paid by Golden Key could not be sustained. They would have also known that it was not registered with the Central Bank. But then again, the company had been in existence since 1978, and the collapse of the Ceylinco Empire had been predicted for more than a decade. You can run a pyramid scheme for so long, only if new depositors keep depositing money in.

After 10 years of agitation the depositors were paid by the Central Bank with funds from liquidated assets of the collapsed venture.

What is important to note is that most of these company founders were well-respected businessmen in Sri Lanka.

Justin Kotalawala the founder of Ceylinco insurance was a well-respected businessman in the country. He was related to one-time prime minister Sir John Kotalawala.

Sakvithi Ranasingha was a private tuition master highly respected by his students and their parents. He abused his reputation to deceive the unsuspecting depositors and lived a lavish life. In fact, he taught English to prisoners while in jai.

Late E.A.P Edirisinghe and his spouse Late Soma Edirisinghe – Desha Bandu Desha Shakthi and a Honorary Doctorate from Open University of Sri Lanka, an unparalleled feat of being awarded the “Lion of the year” on four occasions and many more, were entrepreneurs who would never have resorted to deception. They were pawn brokers, jewellers, film producers, cinema and TV channel owners and philanthropists. The ETI finance matter is sub judice and, therefore, will not be discussed any further.

Late Kattar Aloysius, the founder of Free Lanka Trading company, a well-known businessman in the country who was initially a major exporter of dried fish, but subsequently diversified into industrial products, granite, indenting agent for importing commodities to Sri Lanka, agents for alcoholic beverages such as cognac, Dewar’s whisky, etc. He was respected among the business circles here and abroad.

Now, the name of Aloysius is synonymous with the Treasury bond scams.

As you sow so shall you reap.

Recently, we all held our breath when a conflict began to develop very close to Sri Lanka. The sinking of the Iranian frigate IRIS Dena in the Indian Ocean took place in international waters about 30 miles from Sri Lanka’s southern coast. As the whole world watched, the President and the Government of Sri Lanka were faced with a humanitarian crisis. A second Iranian ship was also in distress and needed assistance. Although Sri Lanka’s maritime history dates back to 5th

Century BCE, this type of geopolitical crisis has been very rare.

Sri Lanka considered it the moral responsibility of the country to help out those affected during this geopolitical crisis. It chose to activate its role as a custodian of the Indian Ocean. Perhaps, not many individuals are aware of Sri Lanka’s historical role in calling on the United Nations to declare the Indian Ocean a Zone of Peace. In 1971, under the leadership of the first woman prime minister of the world, Sirimavo Bandaranaike, Sri Lanka, together with Tanzania brought forth a resolution to the 26th Session of the General Assembly of the United Nations to declare the Indian Ocean a “Zone of Peace.” This was done to avoid it being used by superpower rivalries to gain military control of the region. Sri Lanka’s Ambassador Shirley Amarasinghe, the President of the 31st general Assembly of the UN was responsible for working on this resolution as with others dealing with the “Law of the Sea”.

Chandra Fernando, Educational Consultant, USA)

Wars often produce moments when leaders feel compelled to seek a decisive stroke that will end the conflict once and for all. History shows that such moments can generate choices that would have seemed unthinkable only months earlier. When Harry S. Truman authorised the atomic bombings of Hiroshima and Nagasaki in 1945, the decision emerged from precisely such wartime pressures. As the conflict involving the United States, Israel and Iran intensifies today, the world must ensure that a similar moment of desperate calculation does not arise again.

The lesson of that moment in history is not that such weapons can end wars, but that once the logic of escalation begins to dominate wartime decision-making, even the most unthinkable options can enter the realm of strategic calculation. The mere possibility that such debates could arise is reason enough for policymakers everywhere to approach the present conflict with extreme caution.

As the war drags on, both Donald Trump and Benjamin Netanyahu will face mounting pressure to produce decisive results. Wars rarely remain confined to their original scope once expectations of rapid victory begin to fade. Political leaders must demonstrate progress, military planners search for breakthroughs, and public narratives increasingly revolve around the need for a conclusive outcome. In this environment, media speculation about “exit strategies” or “off-ramps” for Washington can unintentionally increase pressure on decision-makers. Even well-intentioned commentary can shape the climate in which leaders make decisions, potentially nudging them toward harder, more dramatic actions.

Neither the United States nor Israel lacks the technological capability associated with advanced nuclear arsenals. The nuclear arsenals of advanced powers today are far more sophisticated than the devices used in 1945. While their existence is intended primarily as deterrence, prolonged wars have historically forced strategic communities to examine every available option. Even the discussion of such possibilities is deeply unsettling, yet ignoring the pressures that produce such debates can be dangerous.

For that reason, policymakers and societies on all sides must recognise the full range of choices that prolonged wars can place before leaders. For Iran’s leadership and its wider strategic community, absorbing this reality may be essential if catastrophic escalation is to be avoided. From Tehran’s perspective, the conflict may well be seen as existential. Yet history also shows that wars framed as existential struggles can generate the most dangerous strategic decisions.

The intellectual climate in Washington has also evolved. A number of influential voices in Washington now argue that the United States has become excessively risk-averse and that restoring global credibility requires a more assertive posture. Such arguments reflect a broader shift toward the language of renewed deterrence and strategic competition. Yet this very logic can make it politically harder for leaders to conclude conflicts without visible demonstrations of strength.

The outcome of this conflict will also be watched closely by other major powers. In 1945, the atomic decision was shaped not only by the desire to end a brutal war but also by the strategic message it sent to rival states observing the emergence of a new geopolitical era. Today, other significant powers will similarly draw lessons from how the United States manages both the conduct and the conclusion of this conflict.

This is why cool judgment is essential at this stage of the war. Whether the original decision to go to war was wise or ill-advised is now largely beside the point. Once a conflict has begun, the overriding priority must be to prevent escalation into something far more dangerous.

In such moments, the international system can benefit from the quiet diplomacy of actors that retain a degree of strategic autonomy. Among emerging nations, India stands out as a major emerging power in this regard. Despite its energy dependence on the Gulf and deep economic engagement with the United States, India has consistently demonstrated a capacity to maintain independent channels of communication across geopolitical divides.

This unique positioning may allow New Delhi to explore, discreetly and without public fanfare, avenues for de-escalation with Washington, Tel Aviv and Tehran alike. At moments of heightened tension in international politics, the world sometimes requires what might be called an “adult in the room”: a state capable of engaging all sides while remaining aligned exclusively with none.

If the present conflict continues to intensify, the value of such diplomacy may soon become evident. The most important lesson from 1945 is not only the destructive power of nuclear weapons but the pressures that can drive leaders toward choices that later generations struggle to comprehend. History shows that when wars reach their most desperate phases, restraint remains the only safeguard against catastrophe.

(Milinda Moragoda is a former Cabinet Minister and diplomat from Sri Lanka and founder of the Pathfinder Foundation, a strategic affairs think tank, can be contacted via email@milinda. This was published ndtv.com on 2026.03.1

by Milinda Moragoda

Dr. B.J.C. Perera (Dr. BJCP) in his article ‘Language: The symbolic expression of thought’ (The island 10.03.2026) delves deeper into an area that he has been exploring recently – childhood learning. In this article he writes of ‘a trilingual Sri Lanka’, reminding me of an incident I witnessed some years ago.

Two teenagers, in their mid to late teens, of Muslim ethnicity were admitted to the hospital late at night, following a road traffic accident. They had sustained multiple injuries, a few needing surgical intervention. One boy had sustained an injury (among others) that needed relatively urgent attention, but in itself was not too serious. The other had also sustained a few injuries among which one particular injury was serious and needed sorting out, but not urgently.

After the preliminary stabilisation of their injuries, I had a detailed discussion with them as to what needed to be done. Neither of them spoke Sinhala to any extent, but their English was excellent. They were attending a well-known international school in Colombo since early childhood and had no difficulty in understanding my explanation – in English. The boys were living in Colombo, while their father would travel regularly to the East (of Sri Lanka) on business. The following morning, I met the father to explain the prevailing situation; what needs to be done, urgency vs. importance, a timeline, prioritisation of treatment, possible costs, etc.

Doctor’s dilemma

The father did not speak any English and in conversation informed me that he had put both his boys into an International School (from kindergarten onwards) in order to give them an English education. The issue was that the father’s grasp of Sinhala was somewhat rudimentary and therefore I found that I could not explain the differences in seriousness vs, urgency and prioritisation issues adequately within the possible budget restrictions. This being the case and as the children understood exactly what was needed, I then asked the sons to ‘educate’ the father on the issues that were at hand. The boys spoke to their father and it was then that I realised that their grasp of Tamil was the same as their father’s grasp of Sinhala!

In the end I had to get down a translator, which in this case was a junior doctor who spoke Tamil fluently; explained to him what was needed a few times as he was not that fluent in English, certainly less than the boys, and then getting him to explain the situation to the father.

What was disturbing was having related this episode at the time to be informed that this was not in fact not an isolated occurrence. That there is a growing number of children that converse well in English, but are not so fluent in their mother tongue. Is English ‘the mother tongue’ of this ‘new generation’ of children? The sad truth is no and tragically this generation is getting deprived of ‘learning’ in its most fundamental form. For unfortunately, correct grammar and syntax accompanied with fluency do not equal to learning (through a language). It is the natural process of learning two/three languages (0 to 5 years) that Dr. BJCP refers to as being bilingual/trilingual and is the underlying concept, which is the title of Dr. BJCP’s article ‘Language: The symbolic expression of thought’.

“Introduction into society”

It is critical to understand at a very deep level the extent and process of what learning in a mother tongue entails. The mother’s voice is arguably the first voice that a newborn hears. Generally speaking, from that point onwards till the child is ‘introduced into society’ that is the voice he /she hears most. In our culture this is the Dhorata wedime mangalyaya. Till then the infant gets exposed to only the voices of the immediate /close family.

Once the infant gets exposed to ‘society’ he /she is metaphorically swimming in an ocean of language. Take for example a market. Vendors selling their wares, shouting, customers bargaining, selecting goods, asking about the quality, freshness, other families talking among themselves etc. The infant is literally learning/conceptualizing something new all the time. This learning process happens continuously starting from home, at friends/relatives’ houses, get-to-gathers, festivals, temples etc. This societal exposure plays a dominant role as the child/infant gets older. Their language skills and vocabulary increase in leaps and bounds and by around three years of age they have reached the so-called ‘language explosion’ stage. This entire process of learning that the child undergoes, happens ‘naturally and effortlessly’. This degree of exposure/ learning can only happen in Sinhala or Tamil in this country.

Second language in chilhood

Learning a second language in childhood as pointed out by Dr BJCP is a cognitive gift. In fact, what it actually does is, deepens the understanding of the first language. So, this-learning of a second language- is in no way to be discouraged. However, it is critical to be cognisant of the fact that this learning of the second language also takes place within a natural environment. In other words, the child is picking up the language on his own. As readily illustrated in Dr. BJCP’s article, the home environment where the parents and grandparents speak different languages. He or she is not being ‘forcefully taught’ a language that has no relevance outside the ‘environment in which the second language is taught’. The time period we (myself and Dr. BJCP) are discussing is the 0 to 5-year-old.

It does not matter whether it is two or three languages during this period; provided that it happens naturally. For as Dr. BJCP states in his article ‘By age five, they typically catch up in all languages…’ To express this in a different way, if the child is naturally exposed to a second /third language during this 0 to 5-year-old period, he /she will naturally pick it up. It is unavoidable. He /she will not need any help in order for this to happen. Once the child starts attending school at the age of 5 or later, then being taught a second language formally is a very different concept to what happens before the age of 5.

The tragedy is parents, not understanding this undisputed significance of ‘learning in/a mother tongue’, during the critical years of childhood-0 to 5; with all good and noble intentions forcefully introduce their child to a foreign tongue (English) that is not spoken universally (around them) i. e., It is only spoken in the kindergarten; not at home and certainly nowhere, where the parents take their children.

Attending school

Once the child starts attending school in the English medium, there is no further (or minimal) exposure to his /her mother tongue -be it Sinhala or Tamil. This results in the child losing the ability to converse in his/her original mother tongue, as was seen earlier on. In the above incident that I described at the start of this article, when I finally asked the father did he comprehend what was happening; his eyes filled with tears and I did wonder was this because of his sons’ injuries or was it because his decisions had culminated in a father and a son/s who could no longer communicate with each other in a meaningful way.

Dr BJCP goes on to state that in his opinion ‘a trilingual Sri Lanka will go a long way towards the goals and display of racial harmony, respect for different ethnic groups…’ and ‘Then it would become a utopian heaven, where all people, as just Sri Lankans can live in admirable concordant synchrony, rather than as a splintered clusters divided by ethnicity, language and culture’. Firstly, it must be admitted from the aspect of the child’s learning perspective (0 to 5 years); an environment where all three languages are spoken freely and the child will naturally pick up all three languages (a trilingual reality) does not actually exist in Sri Lanka.

However, the pleasant practical reality is that, there is absolutely no need for a trilingual Sri Lanka for this utopian heaven to be achieved. What is needed is in fact not even a bilingual Sri Lanka, but a Sri Lanka, where all the Sinhalese are taught Tamil and vice versa. Simply stated it is complete lunacy– that two ethnic communities that speak their own language, need to learn another language that is not the mother tongue of either community in order to understand one another! It is the fact that having been ruled by the British for over a hundred years, English has been so close to us, that we are unable to see this for what it is. Imagine a country like Canada that has areas where French is spoken; what happens in order to foster better harmony between the English and French speaking communities? The ‘English’, learn to speak French and the ‘French’ learn to speak English. According to the ‘bridging language theory of Sri Lanka’, this will not work and what needs to happen is both communities need to learn a third language, for example German, in order to communicate with one another!

Learning best done in mother tongue

eiterating what I said in my previous article – ‘Educational reforms: A Perspective (The Island 27.02.2026) Learning is best done in one’s mother tongue. This is a fact, not an opinion. The critical thing parents should understand and appreciate is that the best thing they can do for their child is to allow/encourage learning in his/her mother tongue.

This period from 0 to 5 years is critically important. If your child is exposed naturally to another language during this period, he /she will automatically pick it up. There is no need to ‘forcefully teach’ him /her. Orchestrating your child to learn another language, -English in this instance- between the ages of 0 to 5 at the expense of learning in his /her mother tongue is a disservice to that child.

by Dr. Sumedha S. Amarasekara

Showers may occur at several places in the Western and Sabaragamuwa provinces and in Galle, Matara and Nuwara-Eliya districts after 2.00 pm.

Fuel price hikes trigger transport disruptions and calls for fare increases

Prof. Peiris honoured by International Institute of Rehabilitation

CMC resumes parking fees

Substandard coal deepens energy crisis, warns former CEB Chief

Sri Lanka, ICRC to develop unified national database for missing persons

‘Dates have the highest sugar content to fight Coronavirus’

Sunday Island 27 December – Headlines

#SundayIsland 17th December – Headlines

Sunday Island – 28th March

Sunday Island Headlines – 21 March

Sunday Island – 21st February – Headlines

-

News5 days ago

News5 days agoCIABOC questions Ex-President GR on house for CJ’s maid

-

News6 days ago

News6 days agoSri Lankan marine scientist Asha de Vos honoured at UNGA opening

-

News6 days ago

News6 days agoAustralian HC debunks misleading travel risk claims for Sri Lanka

-

News4 days ago

News4 days agoBailey Bridge inaugurated at Chilaw

-

Latest News7 days ago

Latest News7 days agoWednesdays declared a government holiday with effect from 18th March

-

News4 days ago

News4 days agoPay hike demand: CEB workers climb down from 40 % to 15–20%

-

News3 days ago

News3 days agoCIABOC tells court Kapila gave Rs 60 mn to MR and Rs. 20 mn to Priyankara

-

Editorial5 days ago

Editorial5 days agoCouple QR-based quota with odd-even rationing