Features

The world welcomes senior home buyers while Sri Lanka shuts the door at 60

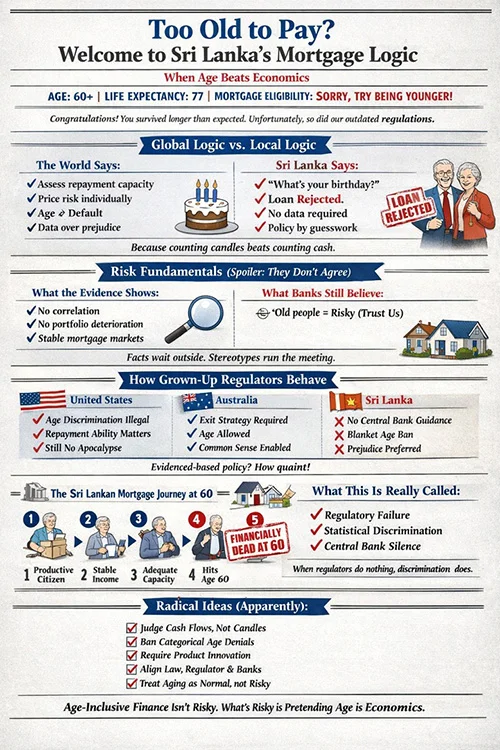

![]() Imagine you are 58 years old, financially stable with a decent pension plan, and finally ready to build your dream home in the suburbs of Colombo. You walk into a bank, application in hand, only to be told: “Sorry, your repayment period would extend past 60. We can’t help you”. In Sri Lanka, this scenario plays out daily, leaving thousands of mature, creditworthy citizens locked out of homeownership. But, step outside our shores, you’ll find a drastically different story.

Imagine you are 58 years old, financially stable with a decent pension plan, and finally ready to build your dream home in the suburbs of Colombo. You walk into a bank, application in hand, only to be told: “Sorry, your repayment period would extend past 60. We can’t help you”. In Sri Lanka, this scenario plays out daily, leaving thousands of mature, creditworthy citizens locked out of homeownership. But, step outside our shores, you’ll find a drastically different story.

From the gleaming towers of Singapore to the countryside cottages of the United Kingdom, older borrowers aren’t just tolerated; they’re actively courted by lenders who understand that age doesn’t determine creditworthiness. While Sri Lankan banks remain trapped in outdated policies that effectively discriminate against anyone over 50, the rest of the world has moved on, creating flexible, dignified pathways for seniors to access home loans.

Role of the Central Bank and the Government

The Central Bank of Sri Lanka has failed in its fiduciary duty by not directing financial institutions to refrain from arbitrarily denying home loans, solely on the basis of age. The Ministry of Finance, therefore, the government, is equally responsible for this failure.

This regulatory vacuum enables systematic discrimination against creditworthy older citizens, contradicting modern banking principles and harming an ageing population desperately needing progressive, not punitive, financial policies.

The Global Picture: Where Age is Just a Number

Many advanced economies, such as the United States and Canada, etc., there is no maximum age limit, whatsoever, for obtaining a 30-year mortgage. The Equal Credit Opportunity Act explicitly prohibits age discrimination, meaning an 80-year-old American can walk into a bank and apply for the same three-decade loan term as a 30-year-old, provided they meet income and credit requirements. Lenders evaluate based on current financial stability, not birth certificates. A 65-year-old Canadian with a solid pension can secure a mortgage extending well into their seventies, with the understanding that income, not age, determines repayment capacity.

Australia sets the typical retirement age benchmark at 65-75, and borrowers, over 65, can still obtain mortgages by demonstrating an exit strategy; a credible plan for repayment that might include downsizing, superannuation funds, or ongoing retirement income. The system acknowledges that life doesn’t end at 60, and neither should financial opportunity.

Global Home Loan Conditions:

A Comparative Analysis

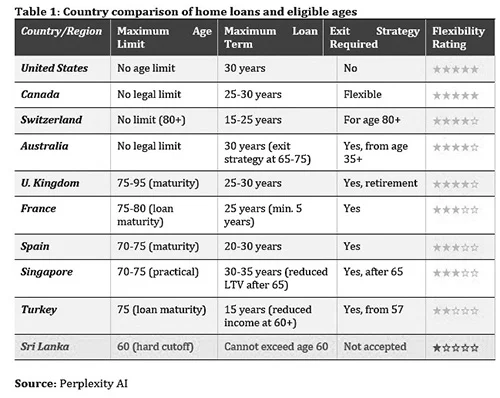

The following table ranks countries from most to least affordable for older home loan applicants, based on maximum age limits, flexibility of terms, and accessibility of financing (Table 1).

What Makes These Systems Work?

The countries at the top of our affordability ranking share several key characteristics. First, they recognise that retirement doesn’t mean financial incapacity. Banks in these countries evaluate total financial health, not just employment status.

Second, they embrace the concept of exit strategies, in Australia, for instance, acceptable exit strategies include downsizing property, selling investment assets, or using superannuation (retirement) funds. These strategies are actually considered and evaluated, not dismissed out of hand. Australian lenders assess whether someone’s superannuation balance is sufficient to clear the debt, or if their investment property provides adequate cash flow. It’s a conversation, not a closed door.

Third, many of these countries offer specialised products for older borrowers. The UK, for example, has retirement interest-only mortgages where borrowers pay only interest during their lifetime, with the principal cleared when the property is eventually sold.

Australia provides reverse mortgages for those aged 60 and above. Under this arrangement, the bank pays the homeowner, rather than the homeowner paying the bank, using the house as security. The full outstanding balance is then recovered when the property is eventually sold.

These may not be perfect solutions, but they represent creative thinking about how to serve an ageing population’s housing needs.

The Hidden Cost of Age Discrimination

Sri Lanka’s rigid age-60 cutoff carries consequences that ripple far beyond individual borrowers. In a nation where life expectancy now exceeds 77 years, we’re telling people they are 17 years of ‘too old’ to be trusted ahead of them. This isn’t just unfair; it’s economically counterproductive.

Consider the broader impact. Sri Lanka has one of Asia’s fastest-aging populations. By 2050, one in four Sri Lankans will be over 60. These aren’t economic liabilities; many are professionals with decades of experience, stable incomes, and substantial assets. A 58-year-old doctor with thriving practice and pension security poses less default risk than a 28-year-old in an uncertain job market, yet our banking system treats them as if the opposite were true.

Learning from Singapore: A Regional

Success Story

We don’t need to look to distant Western nations for alternatives. Singapore, our regional neighbour facing similar demographic challenges, has crafted a more balanced approach. While Singapore’s Monetary Authority hasn’t imposed a hard age limit, banks do apply careful scrutiny to loans extending past age 65.

A Singaporean borrower, over 65, can still obtain financing, but with reduced loan-to-value ratios. If you’re buying a property worth one million dollars and you’re under 65, you might borrow up to 75 percent. Over 65, that drops to 60 percent. It’s more conservative, certainly, but it preserves opportunity.

This approach acknowledges risk without eliminating possibility. It says to older borrowers: Yes, we’ll lend it to you, but we need you to have more equity in the game. Compare this to Sri Lanka’s approach, which effectively says: “We don’t care how much equity you have or how stable your income is, you’re too old”.

A Path Forward for Sri Lanka

The Central Bank of Sri Lanka could issue guidelines similar to Singapore’s loan-to-value adjustments. For borrowers whose loan terms extend past 65, reduce the maximum LTV from 90 percent to 70 or 75 percent.

The Central Bank of Sri Lanka could issue guidelines similar to Singapore’s loan-to-value adjustments. For borrowers whose loan terms extend past 65, reduce the maximum LTV from 90 percent to 70 or 75 percent.

This protects banks from excessive risk while allowing creditworthy older borrowers to access financing. It’s a middle ground that respects both prudent lending standards and individual dignity.

Additionally, Sri Lanka could develop specialised products for its ageing population. Retirement interest-only loans, similar to those in the UK, could serve retirees who have substantial home equity but limited monthly income. Reverse mortgages, properly regulated with strong consumer protections, could help elderly Sri Lankans tap into home equity without monthly payments.

Beyond Banking: A Cultural Shift

Ultimately, changing Sri Lanka’s approach to older borrowers requires more than policy adjustments; it demands a cultural reckoning with how we value our ageing citizens. The countries that lead in age-friendly lending, the United States, Canada, Australia, share a broader commitment to recognising that people can remain economically active and financially responsible well into their later years.

These nations have moved beyond viewing retirement as an endpoint and recognised it as a transition. A 65-year-old today might have 20 or more active years ahead, years in which they’ll continue working part-time, managing investments, drawing stable pensions, and yes, making mortgage payments. Our banking sector needs to catch up to this reality.

Conclusion: Time for Change

As our table demonstrates, Sri Lanka stands alone at the bottom of the global ranking for age-friendly home lending. We’re more restrictive than Turkey with its 15-year maximum terms, more inflexible than Singapore with its sliding loan-to-value scales, and incomparably more rigid than the United States, Canada, or Switzerland, where age barely factors into lending decisions at all.

This isn’t about being soft on risk or abandoning prudent lending standards. Countries with no age limits still assess income, evaluate debt-to-income ratios, and verify creditworthiness. They simply don’t use age as a crude proxy for financial competence. The initiative lies with the Ministry of Finance, which must direct the Central Bank accordingly.

For Sri Lanka’s 58-year-old aspiring homeowner, the current system isn’t just frustrating; it’s a form of systematic discrimination that would be illegal in most developed economies. As our population ages and life expectancy increases, maintaining this policy becomes increasingly untenable. The question isn’t whether Sri Lankan banks will change their approach to older borrowers, but when and how many dreams will be deferred or destroyed in the meantime.

The world has shown us better ways forward. It’s time Sri Lanka joined the 21st century in recognising that 60 isn’t the end of financial opportunity for many, it’s just the beginning.

(The writer, a senior Chartered Accountant and professional banker, is Professor at SLIIT, Malabe. The views and opinions expressed in this article are personal.)

“We are rather respectable in Colombo. We go to bed fairly early, and we remain there till morning. “

According to Sri Lanka’s diplomatic folklore, the late S.W. R. D. Bandaranaike uttered these words while explaining the reasons for Sri Lanka’s abstention on the UN resolution condemning the Soviet invasion of Hungary. Apparently, SWRD’s foreign ministry officials were asleep at home when the diplomatic cable seeking instructions was received from New York. In those days, there were no cell phones, Internet, or even fax or telex machines. The diplomatic cables were sent through post offices. Decoding them was a slow and time-consuming process. Thus, the government could not provide appropriate instructions to our mission in New York in time, and the Sri Lankan delegation abstained on that sensitive UN vote.

Sri Lanka’s Absence from Section 301 Consultations

But then, how does one explain Sri Lanka’s absence from the crucial bilateral consultation held in Washington by the Office of the United States Trade Representative (USTR) during March-April on “Forced Labour” under the Section 301 of the US Trade Act of 1974? Didn’t our foreign and trade ministries send appropriate instructions to Washington in time? Even if the instructions from the foreign ministry were transmitted to our embassy in Washington by pigeon carriers, there was enough time for Sri Lanka to participate in those meetings.

In March, the USTR initiated these 301 investigations on 60 trading partners, and invited all of them for confidential consultations. Out of the 60, 46 participated in these consultations. Sri Lanka was not one of them. Other countries that didn’t participate in these consultations included China, Russia, and Venezuela! In addition to that, the Section 301 Committee conducted a public hearing with interested parties on April 28 and 29. Washington-based diplomats, representatives from few trade ministries as well as representatives from many foreign trade associations and chambers participated in these hearings. Sri Lanka was once again conspicuously absent.

As a result, when the USTR published the proposed forced labour tariffs on June 2nd, Sri Lanka ended up with a 12.5% duty. Pakistani and Indonesian diplomats participated in these consultations and took appropriate follow-up measures, and managed to enter the 10% duty category. As even a threat of a modest tariff hike could disrupt supply chains and reduce competitiveness, particularly in an industry such as garments, I discussed this issue on 15 June and underscored the importance of Sri Lanka’s participation at the next hearing, which was scheduled to be held from July 7th .

Awakening from Diplomatic Slumber and AKD’s Gazette

Fortunately, Sri Lanka finally awoke from weeks of diplomatic slumber, and Ambassador Mahinda Samarasinghe participated in the public hearing on 9 July, and promised, “…. · We have agreed to the text in our negotiations with the USTR on forced labour, …. The gazette as we speak is being printed and I’m getting the gazette tomorrow morning, and the gazette will be shared with USTR as I get it“.

As promised, President Anura Kumara Dissanayake issued a gazette on 10 July banning the imports of goods produced by forced labour. These new regulations are very similar to what Pakistan and Indonesia enacted in April, after their consultations with USTR in March. Why couldn’t we do it in April? Why did we wait till the very last minute?

Challenges ahead

“War is too important to be left to generals alone,” is a famous saying attributed to former French Premier Georges Clemenceau. Similarly, monitoring our main markets is too important to be left to diplomats alone. The United States is the largest single-country market for Sri Lanka. Therefore, Sri Lankan trade chambers and associations should become more proactive in these markets and participate in these events. For example, the chairman of the Pakistani apparel exporters association participated in the April hearings. Similarly, representatives from the Indian Agricultural and Processed Food Products Export Development Authority, the Federation of Indian Chambers of Commerce and Industry, the Confederation of Indian Industry, and Reliance Industries also participated in July hearings. At an event where each speaker is given only five minutes (strictly enforced), having a number of speakers from a country is an advantage. The presence of industry representatives in these kinds of events also help them understand the market dynamics and the future challenges. This is important, particularly because there will be many more challenges with Trump’s tariffs.

With the gazette issued on 10 July, Sri Lanka has imposed a prohibition on the importation of goods produced with forced labour. Now, the challenge will be to effectively enforce the prohibition. And what are the goods produced with forced labour? The USTR list only focuses on aluminum, cotton, electronics, lithium-ion batteries, rice, and tobacco. However, according to the U.S. Department of Labour, the list is much longer. Hence, this list may change continuously during the next two years and tariffs may fluctuate once again.

So, this is definitely not the time to slumber.

(The writer, a retired public servant, can be reached at senadhiragomi@gmail.com)

by Gomi Senadhira ✍️

After the overwhelming grotesquerie of J K Rowling’s latest Cormoran Strike novel (written, I should have noted, as the others were, under the pseudonym Robert Galbraith), I thought I should return to the world of fun, and also a much shorter description since this thriller moves quickly without the layers of detail that Rowling engages in.

I then move to the second comic thriller by Caryl Brahms and S J Simon. This, their second story to feature Vladimir Stroganoff and Adam Quill, was Casino for Sale, as lunatic a romp as the first, though without the emphasis on the ballet that characterized A Bullet in the Ballet.

This one begins with the impresario Stroganoff buying a casino cheap from Baron Sam de Rabinovich, only to find that it was a rundown place, not the grand casino of La Bazouche, a resort on the Frenc+h Riviera, as he had initially thought. The grand one belonged to Lord Buttonhooke, and Stroganoff could not compete, until he thought of bringing the Ballet Stroganoff to the casino – which of course leads to Buttonhooke deciding to have ballet performances in his Casino too.

Stroganoff invites Quill to visit him, which Quill decides to do since he has left Scotland Yard, having come into a legacy. No one believes this, and he has to face questions as to what he did to have been sacked, with sympathy for having been found out.

Caryl and Simon

The day he arrives in La Bazouche there is a murder, of a vitriolic critic called Citrolo, in Stroganoff’s office. He had been going to write a damning review of the opening night of the ballet and Stroganoff, when he realizes Citrolo cannot be swayed, drugs him and dictates the review himself to the papers. He leaves Citrolo sleeping and finds him shot the next morning, whereupon he decides to muddy the waters and leave a suicide note and lots of other murder weapons. So much overkill, as it were, of course ensures that he is arrested.

But the excitable French detective who makes the arrest follows up his suggestion that Buttonhooke was also involved, and so the two casino owners find themselves in cells next door to each other, with the detective Gustave quite happy to provide creature comforts for a fee.

Quill decides he must investigate, and finds Gustave most cooperative, since he has a laid back attitude to work. So it is Quill that finds a notebook which makes it clear Citrolo is an accomplished blackmailer, and that there are lots of possible murderers, including Stroganoff’s croupier, who was crooked, Rabinovich, who was now working for Buttonhooke, a confidence trickster called Kurt Kukumber, whose prospectus for a dud gold mine was found in the office and Prince Alexis Artishok who was engaged in a deal to buy diamonds from the ballerina Dyra Dyrakova.

Stroganoff had been trying to get Dyrakova to dance for him, but having done so previously she had refused. But then to Stroganoff’s chagrin she agreed to dance for Buttonhooke. The clearly crooked Artishok had told Buttonhooke’s mistress Sadie Souse, who was not very bright, that Dyrakova possessed diamonds she was willing to sell cheap, and Sadie was determined to have them.

Quill meanwhile finds out that there was a secret passage to Stroganoff’s office, the obvious solution to what had begun as a locked room mystery, and that this was known by almost everyone apart from Stroganoff himself. And then Rabinovich is murdered, just after Gustave had released his two original suspects, leading him to blame Quill for having insisted on that and thus allowing them to kill again.

Soon afterwards Dyrakova arrives, and the town is full of posters announcing that she will appear in the casinos, elaborate posters for either one, since Stroganoff is determined that she will dance for him, and if she does not come willingly, he has devised a scheme to make her do so unwillingly. So, though Buttonhooke has her taken off to his yacht immediately she arrives at the station, Quill along with Arenskaya gets her into a launch and to Stroganoff’s casino, where she performs to tumultuous applause, not knowing for whom she is dancing.

When Quill asked her about the diamonds, she said she had sold them long ago, and that gave Quill the solution to the mystery. Rabinovich had known about this, and Artishok had killed him to prevent Sadie learning it from him, he had killed Citrolo who had recognized him for an accomplished card sharper, not a Russian prince at all. But before he is arrested, he gets away in a boat, and the police launch that pursues him is on the point of catching him up when it runs out of petrol.

Again, lots of excitement, and entertaining references – Gustave grows marrows – and if not quite as brilliant as its predecessor, Casino was certainly a delightful read.

It was a few years back that a former President of Sri Lanka took it on himself to pronounce SAARC ‘dead’. Since then there have been other sections of Sri Lankan opinion that have joined the critics of SAARC and taken the solemn stance that SAARC has indeed died what may be called a natural death.

It was a few years back that a former President of Sri Lanka took it on himself to pronounce SAARC ‘dead’. Since then there have been other sections of Sri Lankan opinion that have joined the critics of SAARC and taken the solemn stance that SAARC has indeed died what may be called a natural death.

Their fatalism is understandable. SAARC has failed to meet at heads of government or state level for the past several years to take the SAARC process notably forward. Regional cooperation has more or less been only an appealing idea. No substantive concrete projects have taken off to make the idea a hard reality. ‘Inner paralysis’ seems to be SAARC’s lot. Hence the fatalism in these circles.

However, being one of the worst cash-strapped regions of the world and a teemingly populated one with people virtually left to their devices, what choices do the ‘SAARC Eight’ have other than to try their best to band together and continue with their cooperation efforts, however small they may be?

There is no escaping the mounting debt trap for many of these countries and bankrupt Sri Lanka is a glaring example, but ‘throwing in the towel’ and abandoning themselves entirely to the diktats of the strongest economies and their agencies will prove a ‘living death’ for many countries in the SAARC fold.

The gains may be meagre but giving-up on SAARC cooperation in full would prove self-defeating for the organization and South Asia. Right now, the collective intention ought to be to salvage what the region could from the tenuous cooperative efforts. Moreover, such initiatives could go some distance to generate a degree of goodwill among the Eight and help in sustaining a dialogue process.

Given this backdrop it proved ‘a stich in time’ for the Regional Centre for Strategic Studies (RCSS), Colombo, to recently host the SAARC Secretary General Ambassador Md. Golam Sarwar to a round table discussion on the unifying potential of SAARC and its future possibilities, besides other related issue areas.

Held on June 24th and moderated by RCSS Executive Director and former ambassador Ravinatha Aryasinha, the forum brought together a vibrant, wide ranging audience comprising academicians, diplomats, senior public servants, civil society activists and many others. Following the presentation by Ambassador Golam Sarwar titled, ‘Reigniting SAARC: Achievements, Challenges and the Way Ahead’, a lively Q&A followed.

The above forum could be described as an act of lighting the proverbial ‘candle’ rather than ‘cursing the darkness.’ It surely is a ‘darkness’ that could be seen as daunting considering that the region’s pivotal powers, India and Pakistan, are failing to act in a spirit of accord but are engaged in bitter finger-pointing on a number of questions of vital importance to SAARC.

On the other hand, what is the rest of the region doing to bring the above sides together? It is disappointing that to date the rest of SAARC has failed to launch a major diplomatic drive to bring peace between the feuding regional heavyweights. It needs to act without delay and establish its earnestness and this effort would need to prove SAARC’s staying power in the unfolding months and even years.

In assessing SAARC’s seeming failure local opinion in particular has failed to factor in what could be described as weak leadership. Since Sheikh Mujibur Rahman of Bangladesh, the founding father of SAARC, the region has failed to produce a visionary leader who could advance the SAARC cause with charisma and drive.

Among other reasons, weak leadership accounts considerably for the faltering and stuttering status, as it were, of SAARC. Badly needed are leaders who could go the extra mile, think less of narrow national interests and work diligently towards the collective well being of the region but SAARC’s millions of ordinary people have been made to wait in vain for leaders of such stature. Instead, they have been burdened with politicians who seem to be relishing the apparently moribund state of SAARC.

Looking back, it could be said that it was the dynamic leadership factor that led to the launching of the Non-Aligned Movement and for its sustenance for a few decades. True, it could be seen in some quarters that NAM is no more, but as in the case of SAARC, the former too has been unfortunate to be burdened over the years with politicians who lack the vision and drive to unflaggingly advance the fortunes of the South. NAM and SAARC lack the dynamism and vision of leaders of the stature of Jawaharlal Nehru, for example, to give them the required guidance and intellectual depth.

The reasons are complex for there not being among us currently political leaders with the vision and the steadfast commitment to advance the legitimate interests of the South. However, it could be stated with conviction that the majority of Southern leaders have too easily caved in to the demands of the global North and its financial agencies.

These leaders have failed to see, for instance, that the largely market economy oriented Northern governments would not view with favour a centrist economic model that attaches priority to the interests of the dis-empowered publics of the South. This realization ought to have dawned on the current government in Sri Lanka, for instance, some while ago but it has no choice but to abide by IMF dictates since economic survival at present is unthinkable without the latter’s succour.

Accordingly for SAARC this should be the time for some soul-searching. Priority needs to be attached to ending the feuding between India and Pakistan since at present the material fortunes of the region hinge largely on these regional giants giving peaceful relations among them a try. This is no easy challenge to meet but some daring, visionary diplomacy needs to take hold among the rest of SAARC.

There is some sense in SAARC bringing the peoples of the region together through programs that address their best collective interests. A meeting of minds among SAARC nations could enable SAARC and its agencies to build a region-wide people’s movement for progressive political and economic change that could in turn lead to the region’s political leaders sensitizing themselves more to the neglected needs of their publics.

However, the time is ‘now’ for the initiation of these progressive changes and the voice of SAARC well wishers would need to drown out those of their critics.

Former IGP C.D. Wickramaratne found dead at his residence

Venezuela earthquake: Number of known dead rises to nearly 5,000 victims

A few showers may occur in the Western, Sabaragamuwa and North-western provinces and in Kandy, Nuwara-Eliya, Galle and Matara districts

Harmer, Markram and Wolvaardt win top honours at CSA awards

War of words erupts between Minister Chandrasekar and Archchuna in North

Cardinal seeks dismissal of Sallay’s petition

‘Dates have the highest sugar content to fight Coronavirus’

Sunday Island 27 December – Headlines

#SundayIsland 17th December – Headlines

Sunday Island – 28th March

Sunday Island Headlines – 21 March

Sunday Island – 21st February – Headlines

-

Features5 days ago

Features5 days agoPrison riots and politics: NPP’s biggest challenge and Sri Lanka’s biggest opportunity

-

Editorial6 days ago

Editorial6 days agoWhat’s the world coming to?

-

Features2 days ago

Features2 days agoDirty Money

-

Editorial5 days ago

Editorial5 days agoMuch ado about crime: Fish or cut bait

-

Features5 days ago

Features5 days agoMore on Saudi Arabia: ARAMCO and beyond

-

Latest News3 days ago

Latest News3 days agoOil prices hit 1-month high as US-Iran attacks dim Strait of Hormuz outlook

-

Midweek Review2 days ago

Midweek Review2 days agoThe sordid tale of theft and tragedy at Finance Ministry

-

Features4 days ago

Features4 days agoDeepening Democracy – Constitutions and Constitutionalism